Connect with us

Connect with us

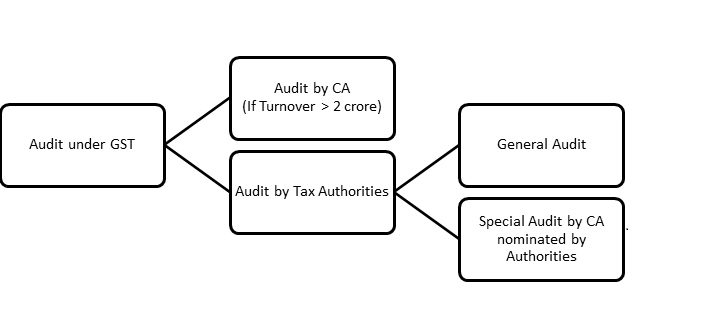

Audit under GST means the examination of records, returns and other documents maintained by the taxpayer to check the accuracy of turnover declared, taxes paid and to assess the compliance with the provisions of GST.

- No audit is required for businesses with turnover less than INR 2 crore.

- Audit by a CA: Every taxpayer with revenue exceeding the prescribed limit of INR 2 crore during a financial year shall get his accounts audited by a Chartered Accountant or a Cost Accountant.

- Audit by tax authorities: As per Section 65 of the CGST / SGST Act, the Commissioner or any officer of CGST or SGST or UT GST authorized by him by a general or specific order, may conduct audit of any registered / enlisted individual.

- Special audits: If at any stage of investigations or any other proceedings, department is of the opinion that the value has not been correctly declared or credit availed is not within the normal limits, department may order special audit by Chartered Accountant or Cost Accountant, nominated by department.